When buying a new dream home, if you are actively researching the fierce debate of MLTA vs MRTA Malaysia, you have just dodged a massive financial bullet. When you sit down to sign your massive RM1 Million housing loan, the banker will almost forcefully push you to buy their MRTA (Mortgage Reducing Term Assurance).

They will tell you it’s “cheaper” and “easier” because they roll the premium into your total loan. But here is the terrifying, unspoken truth of the Malaysian banking industry: MRTA is expressly designed to protect the Bank, NOT your family.

If you want to actually shield your spouse and children from the horror of having their beloved home mercilessly auctioned off by the bank when you die or suffer a Total Permanent Disability (TPD), you must deeply understand MLTA (Mortgage Level Term Assurance).

*(Industry Note: While banks sell MRTA, insurance agents normally sell robust Life Insurance policies structured specifically to act as your MLTA).*

Here are 3 shocking reasons why MLTA absolutely obliterates MRTA.

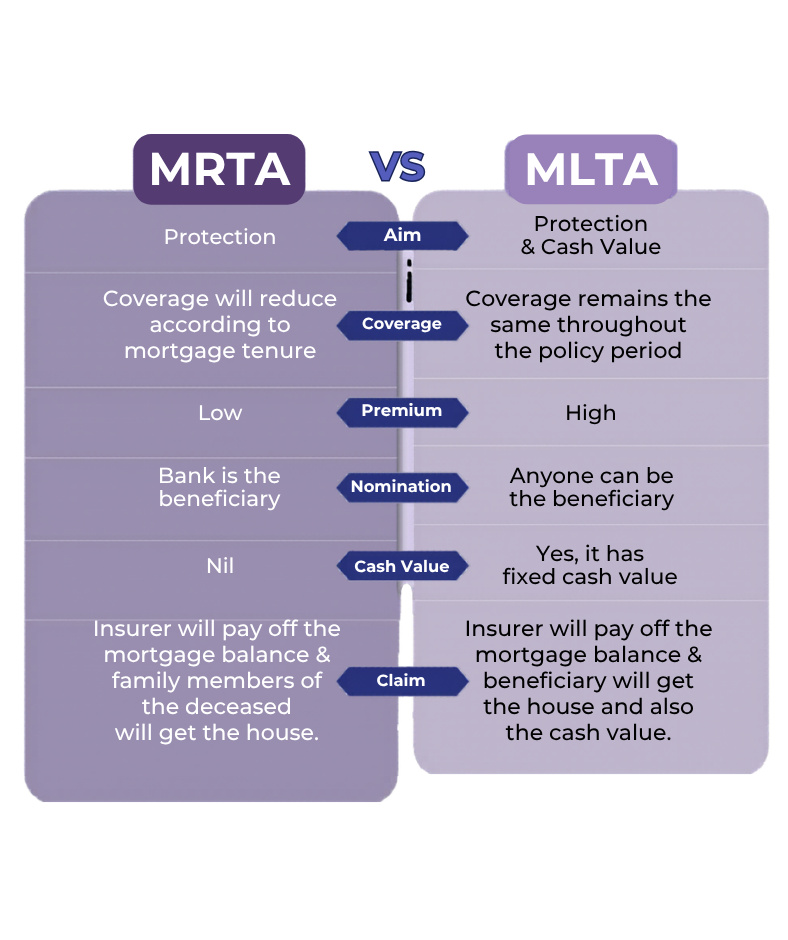

1. MLTA vs MRTA Malaysia: MRTA Shrinks to Zero; MLTA Pays Millions

The “R” in MRTA stands for *Reducing*. This is the biggest invisible trap. As you slowly pay off your housing loan over 30 years, the coverage value of your MRTA mathematically drops down to zero. If you die in year 25, the bank simply clears the tiny remaining loan balance. **Your grieving family receives absolutely RM0.00 cash.**

However, an MLTA operates on a *Level* coverage basis. If your policy covers you for RM1.5 Million, it tightly maintains that RM1.5 Million shield for the entire agreed term! If you pass away in year 25 when you only owe the bank RM200,000, the full RM1,500,000 is released. Your spouse uses RM200k to instantly kill the bank loan, and pockets a massive RM1.3 Million in pure, tax-free cash to send the kids to university and survive!

2. You Can Physically Move an MLTA to Your Next House

An MRTA is completely, hopelessly chained to your specific property and your specific bank. If you sell that house in 7 years to upgrade to a bigger bungalow, or if you intensely refinance your loan to another bank for a better interest rate, your old MRTA is destroyed. You must surrender it and frustratingly buy a brand new MRTA at your new older, more expensive age.

With an MLTA, you physically *own* the policy. It is tied to YOU, the human, not the concrete bricks of the house. When you sell your apartment and buy a RM2 Million semi-D, you simply carry your MLTA policy with you! You do not need to do any new medical check-ups. You completely bypass the new expensive bank insurance. It is the ultimate highly-portable real estate shield.

3. The Brilliant Cash Value Refund Trapdoor

Because MRTA is a cheap “Term” insurance designed by bankers, the money is literally burned. When your 30-year loan ends, you get nothing back. The banker laughs all the way to their bonus.

An elite MLTA is almost always backed by high-performing life insurance tools (like an Investment-Linked Policy or Endowment). This means a powerful portion of your premium is relentlessly deposited into investment funds. After 20 or 30 years, when you finally pay off your house, your MLTA has secretly grown a massive cash value. When comparing MLTA vs MRTA Malaysia, getting your house coverage completely for “FREE” makes the MRTA look like a total scam!

Frequently Asked Questions

Q: Can the bank illegally force me to buy their MRTA if I already intend to use an MLTA?

A: Absolutely NOT! Bank Negara prohibits banks from forcing customers to buy their in-house MRTA. If you show the banker you have a robust MLTA vs MRTA Malaysia setup (usually via a life policy), you can legally assign the policy to the bank to secure the loan. If the banker threatens to reject your loan, report them to Bank Negara instantly!

Do not let a greedy banker trick you into signing an MRTA that shrinks to zero and leaves your family penniless. A house is meant to protect your family, not burden them.

Click the WhatsApp button immediately to request an urgent Mortgage Policy Audit.

I will personally structure a flawless RM1 Million MLTA solution (using the best life insurance framework) that acts as an ultimate, portable real estate shield specifically ensuring your spouse and kids will NEVER lose their home!