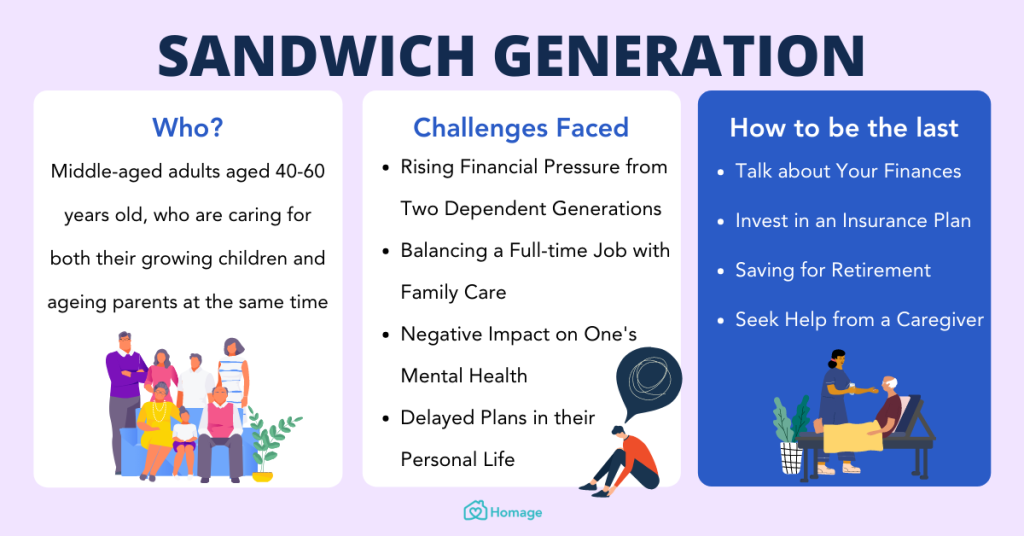

The Crushing Weight of the Middle

As your “Big Sister” in finance, I have seen many successful 35-year-olds walk into my office close to tears. They are earning a good salary in KL or Penang, yet they have zero savings left at the end of the month. Welcome to the reality of the sandwich generation insurance Malaysia trap.

You are squeezed from the top and the bottom. You are paying for your children’s daycare and education, while simultaneously funding your aging parents’ retirement because they didn’t save enough. Let’s talk about the single biggest threat to your sanity and wealth, and how to fix it. *(For more on retirement goals, check out our guide on [Retirement Savings Needed Malaysia 2026].

Sandwich Generation Insurance Malaysia: Why the Trap is so Dangerous

According to the Department of Statistics Malaysia (DOSM) Malaysia is rapidly becoming an aging nation. This means you will likely spend more years taking care of your parents than your grandparents did. When we discuss sandwich generation insurance Malaysia, the core issue is an unexpected medical crisis.

Imagine this scenario:

* You finally saved RM 30,000 for your child’s future university fund.

* Suddenly, your 65-year-old father, who does not have a medical card, suffers a heart attack. The private hospital bill is RM 50,000.

* Government hospitals have a 4-month waiting list for bypass surgery. You cannot wait.

What do you do? You wipe out your child’s education fund. You take on personal loans. The financial trauma of one generation instantly destroys the financial security of the next. This is why sandwich generation insurance Malaysia planning is not optional—it is a survival mechanism.

The “Big Sister” Blueprint to Breaking the Cycle

You cannot stop your parents from aging, but you can shield your own bank account from their medical inflation. Here is how proper sandwich generation insurance Malaysia strategies can rescue your M40 lifestyle:

1. Secure a Medical Card for Your Parents: Even if it is a plan with a deductible or co-payment to keep premiums low, having a RM 1 Million annual limit for your parents means you will never have to choose between their life and your child’s tuition fees.

2. Massive Income Replacement for Yourself: If *you* fall ill, the entire family tree collapses. You need a Critical Illness payout (like PRUWealth Enrich) that is at least 3 to 5 times your annual salary. This ensures your parents and kids keep eating even if you cannot work.

Conclusion: Stop the Financial Trauma Today

Being a good son or daughter does not mean going bankrupt. A solid sandwich generation insurance Malaysia portfolio creates a firewall between your parents’ health risks and your children’s future wealth. Do not wait for a midnight emergency call to realize you are exposed.

FAQ on M40 Family Planning

Q: Are premiums for elderly parents very expensive in a sandwich generation insurance Malaysia setup?

A: They can be higher, but new Bank Negara guidelines allow for Medical Cards with deductibles (e.g., you pay the first RM 1,000, insurance pays the rest). This drastically lowers the monthly premium while still protecting you from a catastrophic RM 100,000 bill.

Q: Can I use my EPF to buy insurance for my parents?

A: Currently, EPF i-Lindung is primarily designed for yourself and your immediate spouse or children. Protecting your parents usually requires using your active daily cash flow. This is exactly why early financial planning is absolutely critical for the sandwich generation in Malaysia before any sudden health crisis strikes.

Are you feeling the pressure of the sandwich generation insurance Malaysia trap?

Click below for a Free “Family Firewall Audit.”

Let’s review your parents’ coverage and protect your children’s future today.