The Danger of Dying Without a Will

Understanding the Malaysia Inheritance Law Distribution framework is the absolute most important step you can take today to protect your family’s future. For high-net-worth professionals and business owners in Kuala Lumpur and Penang, assuming your spouse automatically inherits 100% of your bank accounts and properties when you pass away is a catastrophic financial mistake.

If a non-Muslim Malaysian passes away without a written Will (dying “intestate”), their assets are immediately frozen by the government. The distribution of these frozen assets is strictly dictated by the Distribution Act 1958. Let’s break down exactly what the legal distribution ratios are, why the freezing process is a nightmare for your loved ones, and how elite financial planning can bypass this law entirely.

*(To read the full legal text of the Distribution Act 1958, visit the [External Link]).*

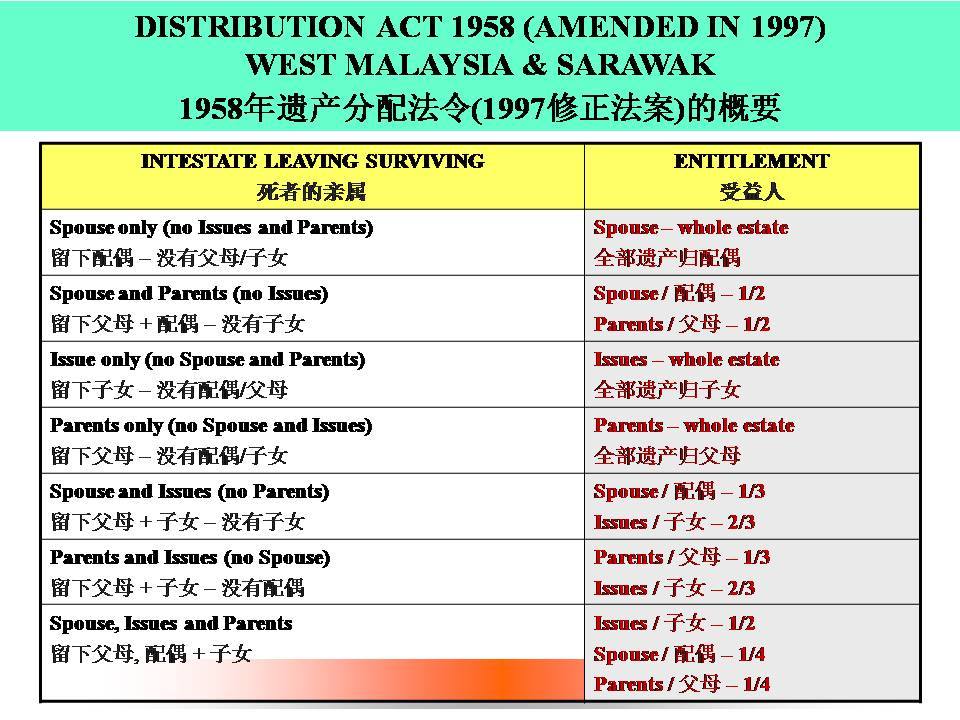

The Exactly Defined Distribution Ratios

Under the Malaysia Inheritance Law Distribution (Distribution Act 1958 for non-Muslims), your assets are divided mechanically based on who survives you.

Here are the precise legal formulas applied to your estate:

Scenario A: Only Spouse Survives

100% goes to your Spouse. (Your entire estate belongs to your husband/wife).

Scenario B: Spouse and Children Survive

1/3 goes to your Spouse.

2/3 is divided equally among your Children.

Scenario C: Spouse, Children, and Parents Survive

1/4 (25%) goes to your Spouse.

1/2 (50%) is divided equally among your Children.

1/4 (25%) goes to your Parents.

Scenario D: Only Parents Survive

100% goes to your Parents.

*(If you fall under Muslim Syariah law, your assets are distributed via the Faraid system. [Post here] to learn how Hibah overrides Faraid).*

The 3 Best Ways to Completely Bypass the Distribution Act

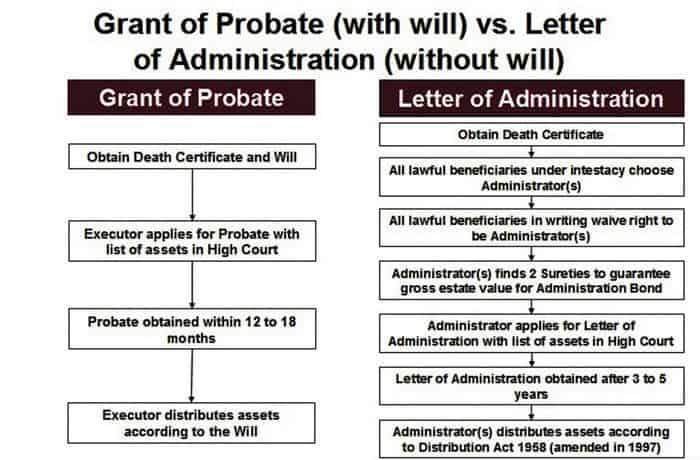

While the Malaysia Inheritance Law Distribution ratios seem fair, the brutal reality is that unlocking an intestate estate (without a Will) requires obtaining a Letter of Administration (LA) from the High Court. This legal process is a nightmare—it typically takes 2 to 5 long years before your family sees a single Ringgit. During this time, your bank accounts are locked, but the bank still demands that your spouse pays the monthly housing mortgage!

Here is how smart professionals bypass this 5-year freeze:

1. Write a Comprehensive Will

Having a written Will immediately upgrades your legal process. Instead of needing an Administrator, you appoint an Executor, and the court grants a Grant of Probate (GP) much faster (usually 3 to 6 months). More importantly, a Will lets you completely overwrite the rigid government distribution ratios and give 100% of your assets to whomever you choose.

2. Life Insurance Nominations

This is your most powerful tool. The money inside a life insurance policy (e.g., a RM2 Million payout) completely bypasses your Will and the Malaysia Inheritance Law Distribution act. By naming your spouse and children as “Trust Nominees,” the insurance company legally dumps the pure cash directly into their bank accounts within 14 to 30 days of your passing. This provides the crucial “survival money” they need to pay off debts while waiting years for the High Court to unfreeze your properties.

3. Create an Insurance Trust with PRUWealth Enrich 2.0

If your children are too young to handle a massive cash inheritance, setting up an Insurance Trust ensures the money is managed by a professional trustee body. Elite life insurance plans like PRUWealth Enrich 2.0 have powerful core functionalities that allow you to seamlessly link them into an Insurance Trust layout. Instead of paying out a lump sum, you dictate exactly how and when your children get the money (e.g., dropping RM5,000 monthly for university fees), ensuring your family empire lasts for generations instead of being squandered in a day.

Local Planning FAQ Section

Q: Does my EPF (KWSP) money follow the Distribution Act 1958?

A: No! Like Life Insurance, your EPF bypasses your Will and the Distribution Act. Your EPF money goes 100% to the person you officially nominated through the KWSP form. If you do not make a nomination, only then will it cause a massive headache for your family!

Q: Can I put my aging parents on my life insurance nomination?

A: Yes. Under the Financial Services Act (FSA), nominating a spouse or a child creates a secure statutory “Trust Policy”. If you are single, nominating a parent also creates this legally protected Trust Policy, guaranteeing the money goes safely to them without creditors being able to touch it.

Don’t let the government decide who gets your life’s earnings.

Click below to schedule a Free Legacy Auditing Session in KL or Penang.

We will use Life Insurance tools to instantly bypass frozen asset nightmares.