The BNM Announcement That Confused Everyone

If you have been paying attention to the news or received letters from your insurance company recently, you are probably very confused. As your “Big Sister” in insurance, my WhatsApp has been blowing up with panic over the new Bank Negara medical card copayment Malaysia regulations.

People are asking: *”Does this mean my insurance is useless? Will I have to pay thousands of Ringgit out of my own pocket if I get admitted to the hospital?”*

Today, we are going to break down exactly what this means, why the government is doing it, and how you can strategically navigate this new landscape.

For a broader view of how medical bills impact families, you can also read our previous guide on the [Sandwich Generation Insurance Trap]

Bank Negara Medical Card Copayment Malaysia: How Does It Actually Work?

To understand the Bank Negara medical card copayment Malaysia system, you need to understand the intention behind it. According to the Bank Negara Malaysia (BNM) official directives, the goal is to fight skyrocketing medical inflation by encouraging policyholders to be more mindful of hospital charges.

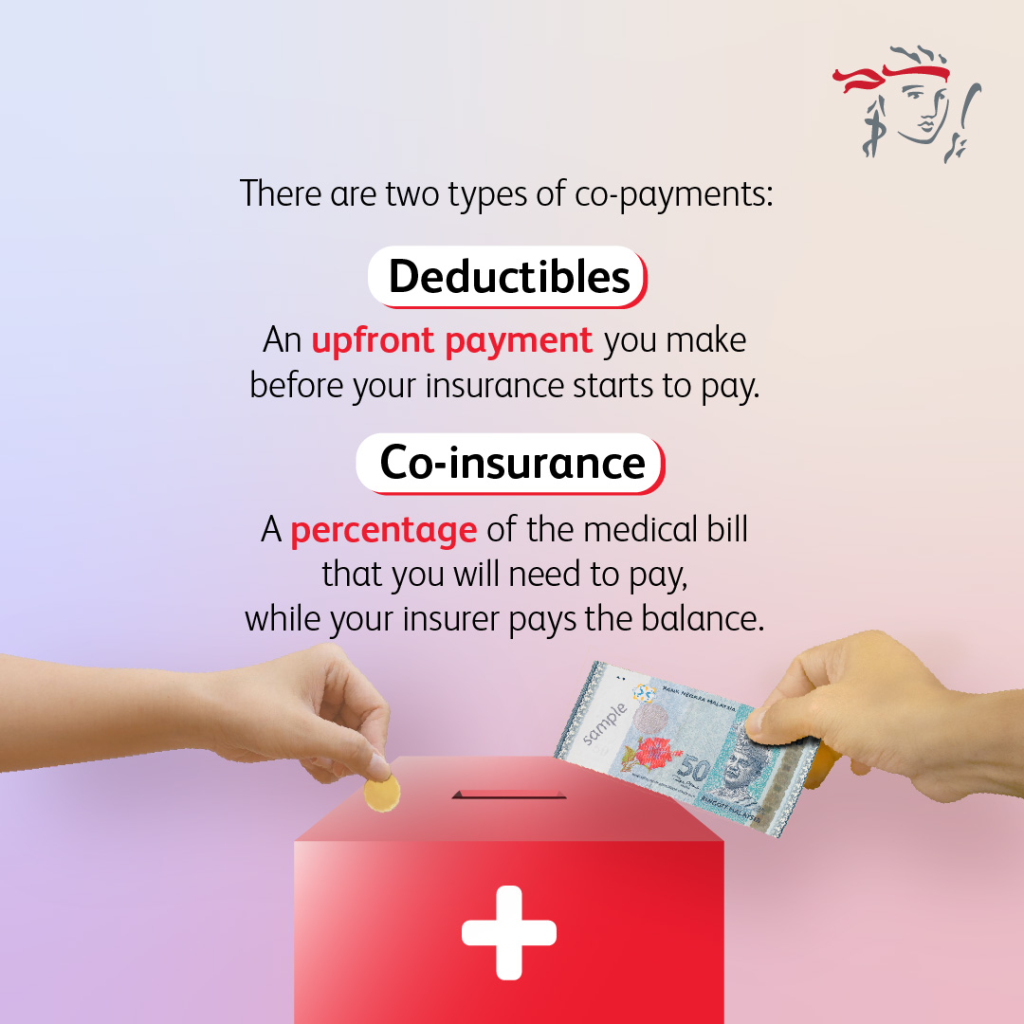

Instead of the insurance company paying 100% of your bill from the very first Ringgit, a co-payment or deductible means you share a small portion of the cost.

Here are the two common ways this is applied in the market:

1. The Percentage Co-Payment (e.g., 5%): If your hospital bill is RM 20,000, you pay 5% (RM 1,000), and the insurance pays the remaining RM 19,000. Most plans have a “cap” (maximum limit) on this co-payment so you don’t go bankrupt on a RM 500,000 bill.

2. The Fixed Deductible (e.g., RM 500 or RM 1,000): Regardless of how big the bill is, you pay the first RM 1,000. The insurance pays everything else. If the bill is RM 50,000, you still only pay RM 1,000.

The Hidden Benefit: Lower and More Stable Monthly Premiums

You might be thinking, *”This is terrible! I am paying for insurance, why should I pay the hospital too?”*

Here is the secret of the Bank Negara medical card copayment Malaysia mandate: It significantly reduces your monthly premium. By agreeing to shoulder a tiny risk (like a RM 500 deductible), the insurance company is able to offer you a massive annual limit (e.g., RM 1 Million to RM 2 Million) at a much cheaper monthly price.

This is especially crucial for families and the sandwich generation who are feeling the pinch of the rising cost of living. Instead of dropping your insurance entirely because the premium is too expensive, you can switch to a co-payment plan. You save hundreds of Ringgit a year on premiums, while still keeping your RM 1 Million safety net fully active for catastrophic illnesses like cancer or heart attacks.

Conclusion: Embrace the Change Strategically

The introduction of the Bank Negara medical card copayment Malaysia rules is a massive shift in how Malaysians view healthcare. It is no longer an “all-you-can-eat buffet.” However, if structured correctly with a professional advisor, a deductible plan is the smartest financial defense you can build.

It keeps your monthly cash flow healthy, protects you against inflation, and ensures that when a true RM 300,000 medical crisis hits, you are 99% covered. Don’t let the new rules scare you—let them empower your financial planning.

FAQ on the New BNM Rules

Q: Am I forced into the Bank Negara medical card copayment Malaysia system for my old policies?

A: No, existing policies with full coverage usually remain untouched unless you choose to upgrade or convert them. However, as medical inflation rises, the premiums for those old full-coverage policies will increase much faster than the premiums for co-payment policies. It is worth reviewing your options.

Q: What if I have an emergency and cannot afford the 5% co-payment?

A: BNM guidelines generally state that co-payments cannot be applied in situations involving emergency treatments at the A&E department or out-patient treatments for critical illnesses like cancer chemotherapy. Your core survival is still fully protected. This is exactly why a thorough consultation is needed before you choose a plan.

Still confused about how the Bank Negara medical card copayment Malaysia mandate affects you?

Click below for a Free “Policy Impact Audit”.

Let’s review your current medical card and see if switching to a deductible plan can save you money!