If you are researching the critical importance of a Life Insurance Nominee Malaysia, you need to confront a terrifying legal reality about what happens the exact second you pass away in this country. Many Malaysians blindly assume that if they die suddenly, their spouse or children can just take their ATM card and easily withdraw the money left behind.

This is a catastrophic misunderstanding that plunges thousands of grieving families into immediate bankruptcy every single year.

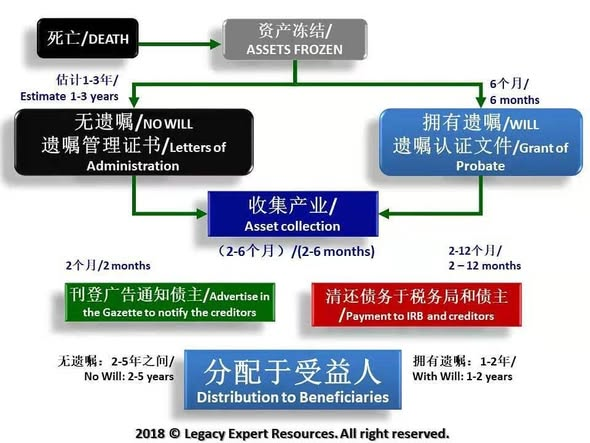

The brutal truth is this: The moment your death cert is issued, Bank Negara heavily mandates that ALL your bank accounts, properties, mutual funds, and fixed deposits are instantly FROZEN. Your spouse cannot legally touch a single cent. To unfreeze this money, your family must hire lawyers and endure a grueling legal process (Probate or Letter of Administration) that can take anywhere from 6 months to 5 agonising years. But how will they eat, pay the mortgage, or survive next week?

This is exactly why your EPF and a watertight Life Insurance Nominee Malaysia structure are the ultimate financial lifelines. Here are 3 shocking reasons why these are the *only* tools you have to bypass the government freeze.

1. The Malaysian “Bypass Rule”: Only 2 Assets Ignore the Freeze

In the Malaysian legal system, there are strictly only TWO financial assets that completely bypass the terrifying frozen probate process: your EPF (Employees Provident Fund) and your Life Insurance payouts.

Everything else goes into your frozen “estate.” But if you have officially named your spouse or children as a Life Insurance Nominee Malaysia, that RM1 Million or RM2 Million death benefit cash does *not* belong to your generalized frozen estate. Legally, it belongs directly to the nominee. This means the money skips the lawyers, skips the courts, skips the government debt collectors, and flies straight into your family’s hands.

2. Instant Cash Injection in 7 to 14 Days

When your bank accounts are locked by the government, your family still needs cash for your funeral, next month’s car loans, and the children’s school fees. They cannot wait 2 years for the High Court to approve a Will!

Because a formal Life Insurance Nominee Malaysia acts as a legally binding, indisputable trust contract, Prudential does not wait for a court order. Upon receiving the death certificate, the insurance company will process and dump the enormous pure cash payout directly into your nominee’s bank account, typically within 7 to 14 working days! This immediate cash injection is exactly what keeps a widow and her orphans out of deep, terrifying debt while the rest of your assets remain stuck in legal purgatory.

3. Creditor-Proof: Your Debts Cannot Steal Their Money

Here is a horrifying fact about leaving a traditional inheritance via bank accounts: Jeśli you die with outstanding debts (credit cards, massive business loans, personal loans), the bank and creditors have the first legal right to rip the money out of your frozen estate to pay themselves off *before* your children get anything. Often, nothing is left.

However, under the Financial Services Act (FSA) 2013, if you name your spouse, child, or parent as a Trust Life Insurance Nominee Malaysia, that multi-million ringgit cash payout is 100% physically protected from your creditors. The banks cannot touch it. Debt collectors cannot sue for it. It is an impenetrable absolute financial shield engineered solely to feed and protect your bloodline.

Frequently Asked Questions

Q: Can I put my sibling (brother/sister) as a Nominee to create a protected Trust?

A: No! According to Malaysian law, heavily protected Trust status for a Life Insurance Nominee Malaysia is *only* created if the nominee is your spouse, child, or parent (if you are single). If you nominate a sibling or a friend, the money simply falls under your standard estate, meaning it is exposed to your creditors, freezes, and is heavily delayed by the probate process.

Q: I wrote my Will. Won’t my Will just automatically override my Insurance Nomination?

A: This is a deadly mistake. A Will does NOT override a Life Insurance Nomination nor your EPF nomination. If you nominated your ex-wife on your Prudential policy 10 years ago, but recently wrote a Will giving everything to your new wife, the massive life insurance cash will *still* be legally paid directly to your ex-wife! You must violently update your Life Insurance Nominee Malaysia forms actively with your agent.

Do not let your spouse starve while lawyers slowly argue over your frozen bank accounts.

You need an impenetrable cash shield.

Click the WhatsApp button below to request an absolutely urgent Policy Audit.

I will personally review your existing policies to ensure your Life Insurance Nominee Malaysia is perfectly structured to bypass probate, shield against creditors, and drop RM1 Million instantly into your family’s hands.