The Rising Epidemic We Cannot Ignore

When we look at national health data, the statistics surrounding cancer in Malaysia are deeply alarming. It is no longer a rare disease that only affects the elderly.

Today, as a professional wealth and risk advisor, I see clients in their 30s and 40s being diagnosed with early-stage breast, colorectal, and lung cancers at an unprecedented rate.

While medical advancements have dramatically improved survival rates for cancer in Malaysia, surviving the disease is only half the battle. The other half is surviving the financial devastation that comes with it.

Today, we must address the objective reality of oncology costs and how proper risk management can shield your life savings. *(For a deeper understanding of critical illness protection, read our guide on [Prudential TMCC Claims]).*

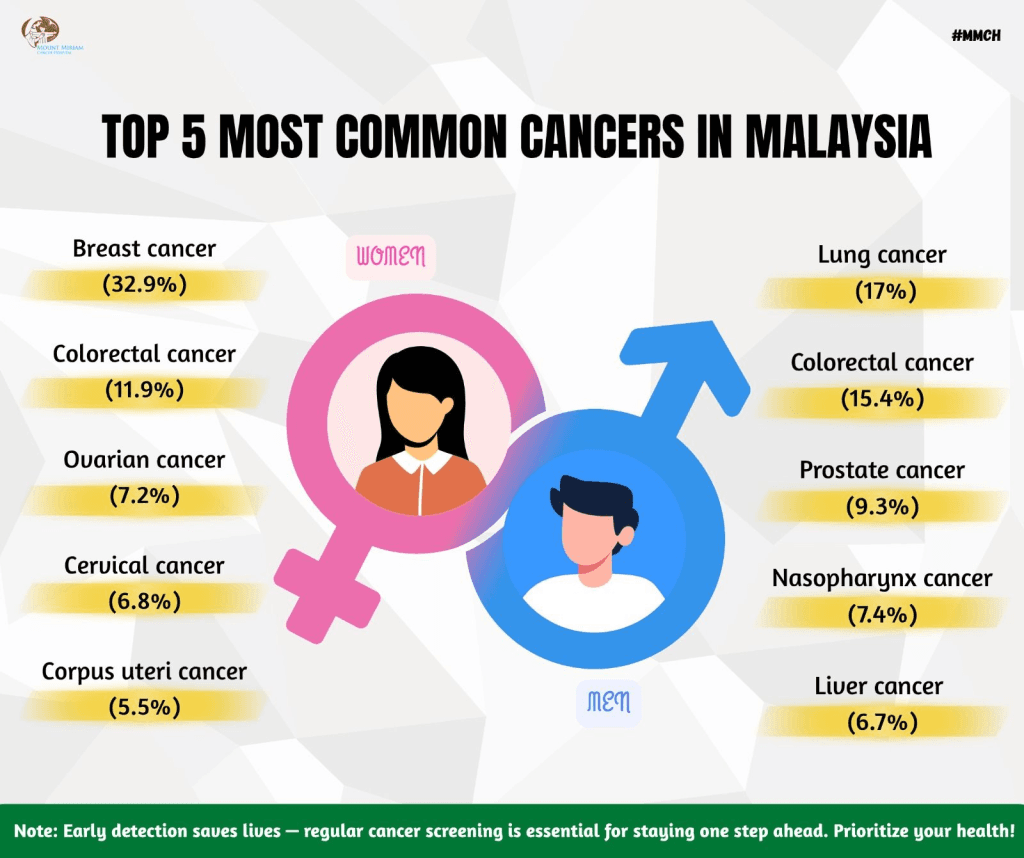

Cancer in Malaysia: The True Financial Cost

According to reports from the National Cancer Society Malaysia (NCSM), cancer remains one of the leading causes of death nationwide. However, what is often not discussed is the astronomical cost of modern treatments.

When dealing with cancer in Malaysia, the billing from a top private hospital (such as Sunway Medical Centre or Gleneagles) can easily dismantle a family’s financial foundation.

Let’s break down the realistic costs:

1. Diagnostic Procedures : PET scans, biopsies, and extensive blood work can cost between RM 5,000 to RM 15,000 before treatment even begins.

2. Surgery and Hospitalization : Depending on the complexity, surgical removal of tumors can range from RM 30,000 to RM 80,000.

3. Targeted Therapy and Immunotherapy : This is where costs skyrocket. Modern cancer drugs are highly effective but can cost RM 10,000 to RM 30,000 *per cycle*. A full year of treatment can easily exceed RM 200,000 to RM 300,000.

If your current medical card only has an annual limit of RM 100,000, it will be exhausted within the first few months of targeted therapy.

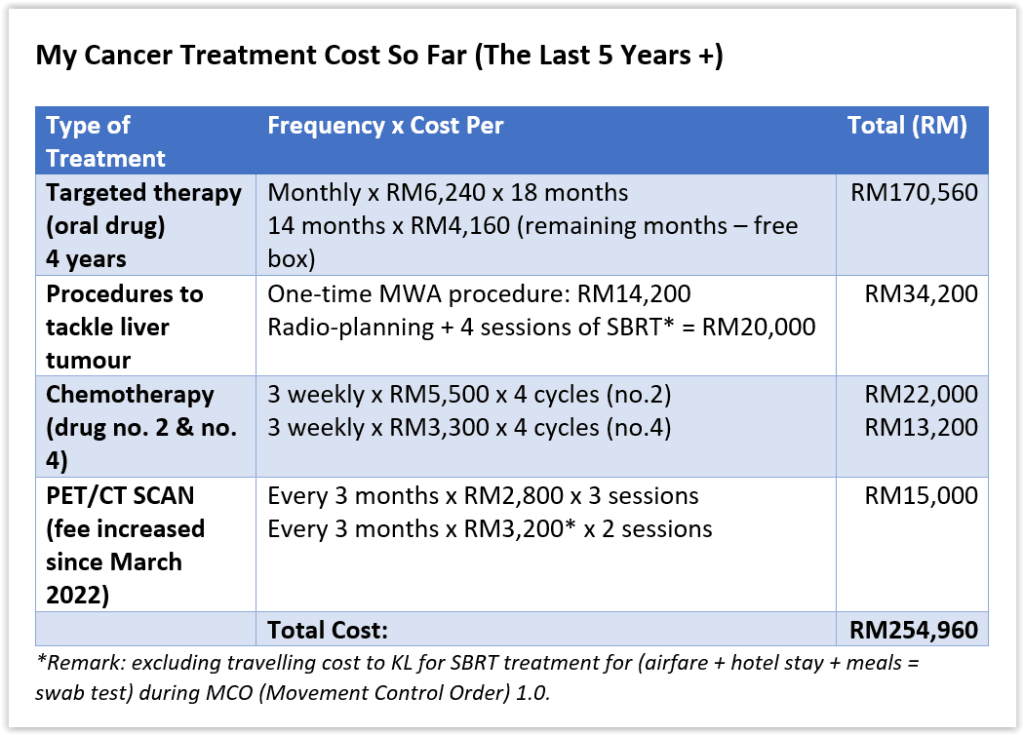

A Real-Life Warning: RM 255,000 in Out-of-Pocket Costs

To understand the devastating reality of cancer in Malaysia, we only need to look at the recent case of Sew Boon Lui, a metastatic breast cancer survivor and patient advocate in Sarawak

When her cancer recurred, she required a targeted therapy drug that was *not* funded by the government hospital. The medication cost over RM 6,000 every single month. Over the course of five years, she paid nearly RM 255,000 completely out-of-pocket from her life savings just to stay alive, accelerating the depletion of her 25 years of hard-earned wealth.

Her story highlights a terrifying gap: Even in public hospitals, advanced targeted therapies for severe cancers are often self-funded. Without a comprehensive medical card, you are completely unprotected against these astronomical bills.

The Hidden Cost: Income Loss

The medical bill is only the first wave of the attack. The second wave is the loss of your income.

Treating cancer in Malaysia requires intense physical and mental endurance. Chemotherapy and radiation often leave patients too weak to work for 6 to 12 months, or sometimes longer. If you are a business owner, your business operations may halt. If you are an employee, your paid medical leave will eventually run out, leading to unpaid leave or job loss.

This is precisely why a high-limit Medical Card is not enough when fighting cancer in Malaysia.

You must pair it with a comprehensive Critical Illness plan (like Prudential TMCC). While the medical card pays the oncology department, the critical illness payout replaces your lost salary, allowing you to pay your mortgage, buy necessary supplements, and maintain your family’s dignity.

Conclusion: Fortify Your Defense Today

The rising incidence of cancer in Malaysia is an objective threat, but it is a threat that can be managed with professional financial planning. Do not wait for a diagnosis to realize your coverage is inadequate. By securing a high-limit medical card with no lifetime limit and a robust income replacement strategy today, you ensure that a medical crisis never becomes a financial disaster.

FAQ on Cancer Coverage

Q: If I survive cancer in Malaysia, can I ever buy insurance again?

A: It is extremely difficult. Most insurance companies will permanently decline an applicant with a history of cancer, or impose strict permanent exclusions. This highlights the absolute necessity of buying maximum coverage *while* you are completely healthy. Once you are diagnosed with cancer in Malaysia, your window to secure new coverage permanently closes.

Q: Does a standard medical card cover outpatient cancer treatments like chemotherapy?

A: Yes, most comprehensive medical cards cover outpatient cancer treatments. However, because modern therapies are so expensive, you must ensure your card’s annual limit is high enough (e.g., RM 1 Million or more) to sustain years of continuous treatment.

The cost of fighting cancer in Malaysia is rising every year. Are you truly prepared?

Click below for a Free “Health Wealth Audit”.

Let’s objectively review your current medical limits and critical illness coverage to ensure your family’s assets are completely shielded.