Passing the Torch, Not the Burden

When we discuss legacy planning with life insurance Malaysia, many people assume it is a topic reserved only for ultra-rich billionaires and tycoons.

As your “Big Sister” in finance, let me correct that misconception right now. If you own a house, have a few bank accounts, and have children, you need a legacy plan.

Leaving behind a legacy is not just about leaving behind money. It is about making sure that the wealth you spent your entire life building actually reaches your children safely, smoothly, and without sparking a family war.

Today, we are going to explore how insurance acts as the ultimate tool for creating generational wealth. *(If you haven’t yet, please read our crucial guide on [Why Bank Accounts Freeze After Death]).*

Legacy Planning With Life Insurance Malaysia: The Unfair Advantage

Why use life insurance instead of just leaving cash in the bank or a house to your kids?

The answer lies in the unique financial leverage and legal structure of a life policy.

According to the Inland Revenue Board of Malaysia (LHDN), life insurance payouts are generally not subjected to income tax.

This makes it an incredibly efficient vehicle.

When you execute legacy planning with life insurance Malaysia, you unlock three “unfair” advantages:

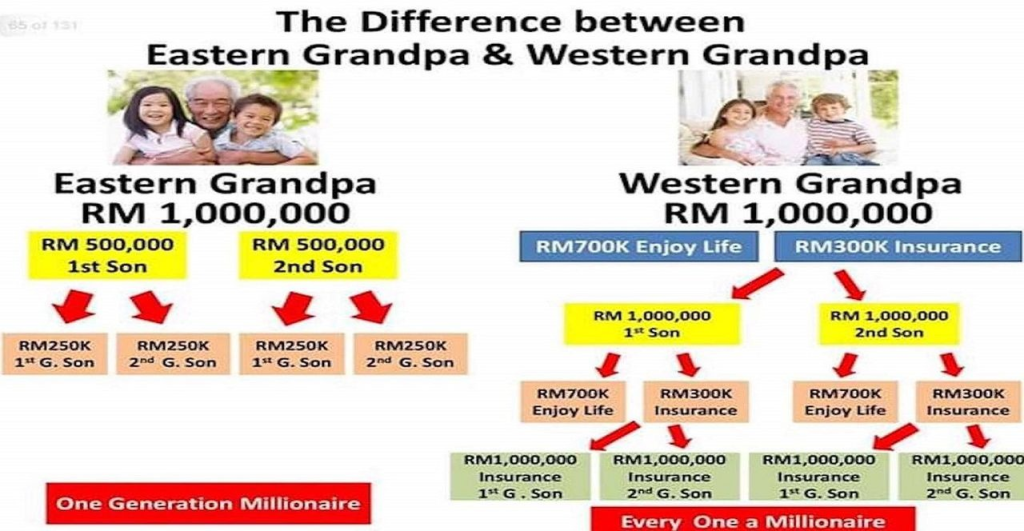

1. The Magic of Leverage

To leave RM 1 Million in cash to your children, you have to literally earn, save, and lock away RM 1 Million in the bank. That takes decades of hard work.

With life insurance, you might only pay a premium of RM 15,000 a year. From day one, you have instantly created a RM 1 Million asset for your family. You are buying time. You are turning pennies into gold bars for the next generation.

2. Equalizing the Inheritance

Imagine you have two children. You own a successful restaurant business worth RM 2 Million, but no cash. Your son wants to take over the restaurant, but your daughter wants nothing to do with it. How do you divide the business fairly without forcing them to sell it?

This is where legacy planning with life insurance Malaysia shines. You leave the RM 2 Million business to your son, and you buy a RM 2 Million life insurance policy naming your daughter as the nominee. Both children receive exactly RM 2 Million. No arguing, no selling of family assets.

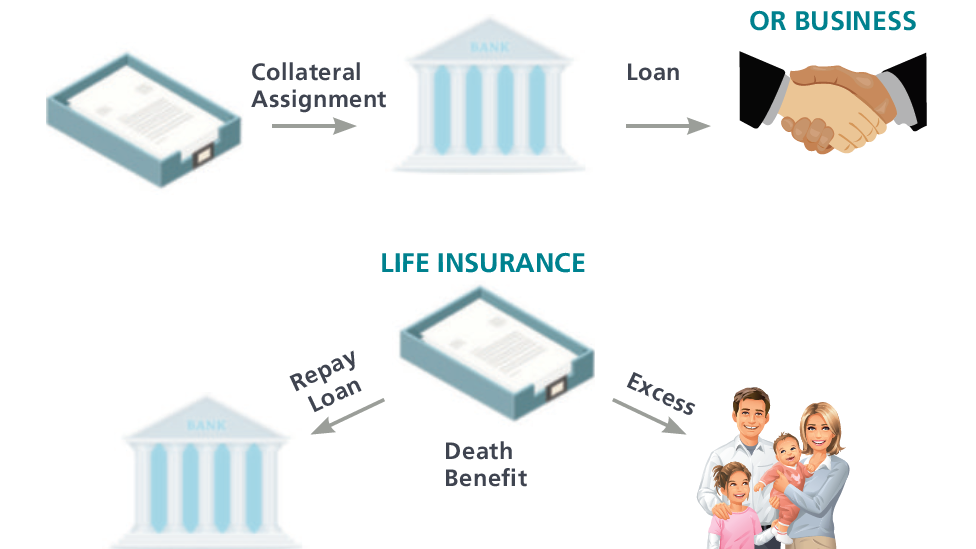

3. Immediate Liquidity

As we discussed in previous posts, properties and bank accounts get frozen during the probate process. A life insurance payout bypasses the will and the frozen estate. It provides instant liquid cash directly to your children so they can pay off the estate administration fees or inheritance taxes for properties overseas.

Conclusion: Build a Dynasty, Not Just a Living

You have worked too hard to let your wealth be diminished by inflation, legal fees, or family disputes after you are gone. Proper legacy planning with life insurance Malaysia ensures that your love and hard work continue to protect and elevate your children and grandchildren long after you have passed.

Let’s build your family dynasty today.

FAQ on Generational Wealth

Q: Can I name my minor children (under 18) as nominees for a life insurance policy?

A: Yes, you can. However, because they are minors, the insurance company cannot pay the money directly to them. Under the Financial Services Act, the money will be paid to a surviving parent or a legally appointed trustee, who must hold the money in trust for the child until they reach 18.

Q: Is legacy planning with life insurance Malaysia only for the ultra-rich?

A: Absolutely not. Even a RM 500,000 policy is a massive legacy for a middle-class family. It can ensure your children graduate debt-free from university or have the capital to start their own business, entirely changing their trajectory in life.

Have you thought about what you are leaving behind?

Click below for a Free “Generational Wealth Audit”.

Let’s design a custom legacy planning with life insurance Malaysia strategy to ensure your children inherit wealth, not complications!