Estate Planning Malaysia: The 3 Crucial Truths You Need to Know

When people hear the term estate planning Malaysia, they immediately think of writing a Will.

While having a Will is absolutely essential to distribute your assets according to your wishes, there is a dangerous misconception that a Will solves all financial problems after death.

As a professional wealth and risk advisor, I often ask my clients: *”A Will takes 6 to 18 months to execute. What does your family eat during those 18 months when all your bank accounts are completely frozen?”*

This is the hidden crisis of estate planning Malaysia.

Today, we will explore the ultimate, probate-free solution: Life Insurance.

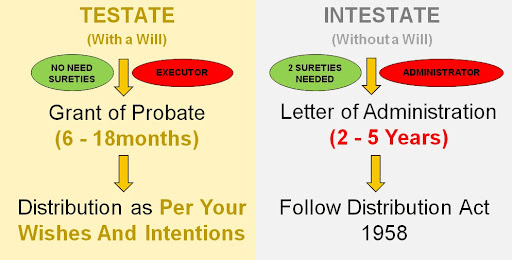

1. The Probate Trap: Why Assets Get Frozen

The moment a person passes away, all their bank accounts, properties, and stock portfolios are legally frozen by the government. This is standard procedure to protect the deceased’s assets.

Even if you have a Will, your executor must apply to the High Court for a Grant of Probate. This legal process is complex, requires hiring lawyers, and can easily drag on for a year or longer depending on the complexity of the estate. During this lengthy period of estate planning Malaysia, your spouse and children cannot withdraw a single Ringgit from your bank account to pay for daily groceries, children’s tuition fees, or utility bills.

*(If you want to understand the devastating impact of this, read our previous guide on [Frozen Bank Accounts After Death in Malaysia]).*

2. The Life Insurance Loophole: Immediate Liquid Cash

Here is the most powerful secret in estate planning Malaysia: Life insurance payouts completely bypass the Will and the lengthy probate process.

Under Schedule 10 of the Financial Services Act 2013 (FSA 2013), if you nominate your spouse, child, or parent (if you are single) as the beneficiary, a legal trust is automatically created.

What does this mean for your family?

It means that within a few short weeks of presenting the death certificate, the insurance company will directly transfer hundreds of thousands (or millions) of Ringgit straight into your family’s bank account.

This provides the crucial liquid cash they desperately need to survive the 18-month freeze while the lawyers sort out the Will.

When we structure proper estate planning Malaysia, a high-coverage life insurance policy is the “bridge” that feeds your family while the Will is being executed.

3. Debt Cancellation: Protecting the Family Home

Before your assets can be distributed to your heirs according to your Will, the law requires that all your outstanding debts be paid off first. This includes personal loans, credit card debts, income tax, and business debts.

If there is not enough cash in your estate to cover these debts, the courts may force the sale of your properties—including the family home where your spouse and children currently live.

Many Malaysians mistakenly believe their MRTA/MLTA is enough.

But MRTA only covers the mortgage balance; it does not leave extra cash for living expenses, and it certainly doesn’t pay off your credit cards. By implementing a life insurance policy within your estate planning Malaysia strategy, you create an instant “Debt Cancellation Fund.”

Your family can use the insurance payout to immediately clear all debts, ensuring the family home is passed down free and clear.

Conclusion: A Will Dictates, Life Insurance Delivers

A comprehensive approach to estate planning Malaysia requires both legal tools and financial tools. Your Will dictates *who* gets what, but your Life Insurance ensures there is actually *immediate cash* to deliver.

Do not leave your family asset-rich but cash-poor.

FAQ on Life Insurance in Estate Planning

Q: If I put my life insurance policy in my Will, does it get frozen too?

A: This is a huge mistake! If you fail to make a proper nomination with the insurance company and instead direct the payout to your “estate” via your Will, the money becomes part of the frozen estate and is subjected to the 18-month probate delay. Always make direct trust nominations with your insurance provider.

Q: Are life insurance payouts subject to creditor claims?

A: Under a proper trust nomination (Schedule 10 of FSA 2013) where a spouse, child, or parent is named, the payout is legally protected from your personal creditors. This ensures the money goes 100% to your family, not to the banks you owe. This is a vital pillar of estate planning Malaysia.

A Will takes over a year to execute.

Does your family have enough instant liquid cash to survive the legal freeze?

Click below for a Free “Estate Liquidity Audit”.

Let’s objectively assess if your life insurance portfolio is robust enough to protect your legacy.