The Ultimate Misconception of “Joint Names”

Understanding the true legal impact of joint property ownership in Malaysia is crucial before you sign any documents.

Congratulations on getting the keys to your new home! For many young married couples, securing a joint property ownership in Malaysia is the ultimate symbol of love and commitment.

You might naturally assume that because both of your names are on the Sale and Purchase Agreement (SPA) and the bank loan, the house is permanently secured for both of you.

But what happens if the unexpected strikes and one spouse passes away prematurely? Does the surviving spouse automatically inherit the other 50% of the property?

The shocking truth about joint property ownership in Malaysia is: NO.

Buying a house together does not mean the house is 100% yours.

The Legal Reality: The 50% Trap

When dealing with joint property ownership in Malaysia, unless specified otherwise, most joint properties are held as Tenants in Common. This means you and your spouse each own a distinct 50% share of the house.

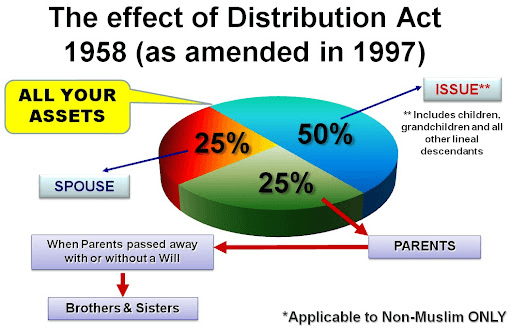

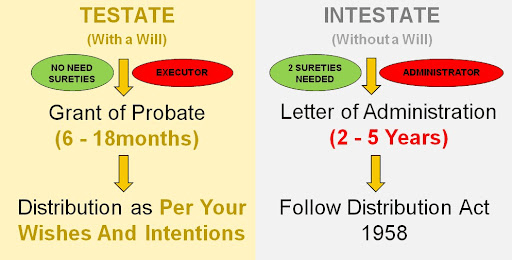

If your spouse passes away without a will, their 50% share is instantly frozen. It does not automatically transfer to you. Instead, according to the Distribution Act 1958, that 50% will be distributed among their surviving parents, children, and you (the surviving spouse).

This legal process of joint property ownership in Malaysia triggers a nightmare scenario for the surviving partner:

- You Cannot Sell the House: Because you only own 50% of the property rights, and the other half is frozen or contested, you cannot sell the house to get cash.

- Sharing with In-laws: You may suddenly find yourself sharing property ownership with your deceased spouse’s parents or siblings.

- The Risk of Auction: If you cannot afford the full monthly mortgage repayment on a single income, the bank will eventually auction off your home.

The Solution: Build a Financial Fortress

Smart adults don’t just sign a mortgage; they build a Financial Fortress to protect their family from the risks of joint property ownership in Malaysia.

The most effective way to secure a joint property ownership in Malaysia is by setting up an MLTA (Mortgage Level Term Assurance) or a dedicated high-coverage life insurance policy, combined with proper estate planning (a Will).

When a crisis occurs, this safety net immediately activates, delivering a large, tax-free cash payout directly to you.

- Buy Out the Remaining 50%: You can use this cash to legally buy out the remaining 50% share from the other family members, gaining 100% complete ownership.

- Clear the Debt: You can pay off the entire outstanding bank loan, ensuring you never have to worry about monthly installments or the bank auctioning your home.

A house is made of bricks, but a home is made of security. Don’t let your dream home become an auction item.

FAQ on Joint Property Ownership

Q: Doesn’t the bank force us to buy MRTA when we sign the loan? Isn’t that enough for joint property ownership in Malaysia?

A: MRTA protects the bank, not your family. If the insured person passes away, the MRTA payout goes directly to the bank to settle the loan. However, it does not solve the legal issue of the frozen 50% ownership under the Distribution Act. An MLTA or personal life policy gives cash to *you*, allowing you to manage the ownership buyout and living expenses.

Q: What if we signed a “Joint Tenancy” instead of “Tenancy in Common”?

A: True “Joint Tenancy” with the right of survivorship is extremely rare for joint property ownership in Malaysia without specific trust structures. Standard SPA agreements almost always default to Tenancy in Common. You must check your specific legal documents, but never assume you automatically inherit the property.

The legal risks of joint property ownership in Malaysia can leave your family homeless if the worst happens.

Are your property and loved ones truly protected?

Click below for a Free “Property Risk Audit”.

Let’s restructure your financial defense to ensure your home stays 100% in your family.